⚠️ WARNING: 47% of nomad accounts frozen in Q1 2026 were due to “VPN Leakage.” Is your balance safe tonight?

In 2026, the greatest threat to a digital nomad isn’t local taxes—it is the “Shadow Freeze.” As global banking regulations tighten, US neobanks like Mercury, Relay, and Wise have deployed aggressive AI compliance filters to detect regional instability. If you are operating from the top 5 geopolitically stable nomad hubs in 2026, you might feel safe, but your bank account is watching your every move. One login from a “high-risk” IP address or a poorly timed KYC (Know Your Customer) check can instantly lock your funds, leaving your business paralyzed.

“With the launch of the 2026 Thailand TDAC system, banks now have real-time data on your location. If you aren’t prepared, your account is a sitting duck.”

The De-Risking Wave of 2026

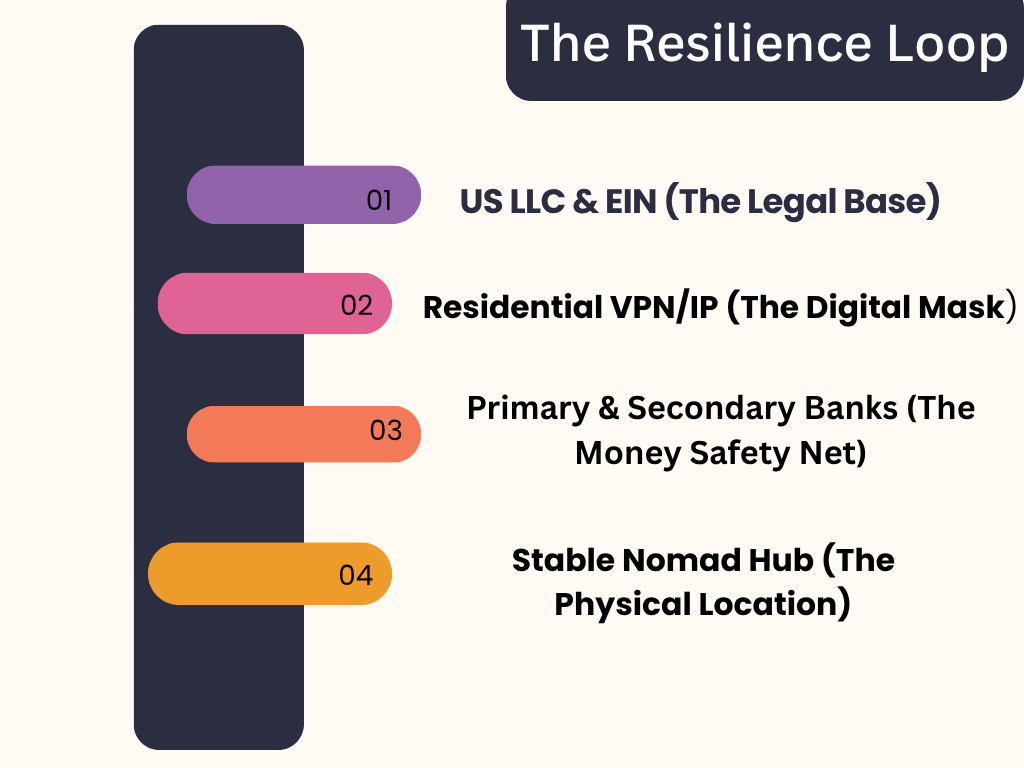

We have entered the era of “Institutional De-Risking.” Banks are no longer just looking for illegal activity; they are looking for complexity. For the IRS and US financial institutions, a nomad who owns a Wyoming or Delaware LLC but lives in Peru or Malaysia represents a “high-complexity” risk. When global tensions rise, banks protect themselves by closing accounts that don’t fit a standard profile. To reach the peak of financial freedom, you must build a “Banking Resilience Stack” that makes your business look stable, even when you are on the move

Why Your EIN is Your First Line of Defense

Most account freezes happen because of a mismatch in data. Your EIN (Employer Identification Number) is your business’s social security number. In 2026, banks are cross-referencing your EIN registration data with your physical login location. If you obtained your EIN without an SSN, your compliance requirements are even stricter. Resilience starts with ensuring your “Tax Stack” is flawlessly documented before the bank sends that dreaded verification email

Whether you are an Irish freelancer or a Norwegian consultant, the 2026 de-risking wave affects us all the same

Updated 2026 Regional Data: Requirements for NZ, German, Norway, Ireland, Canada Residents to Avoid Account Flags

| Country | 2026 Compliance Requirement | Account Freeze “Trigger” | The “Peak” Strategy |

|---|---|---|---|

| New Zealand | NZBN & FATCA Self-Certification | Using NZ-based Wise for large US LLC transfers without a US EIN. | Keep a “Buffer” of $2,000 in a local NZ bank for emergencies. |

| Germany | Steuer-ID & Meldebescheinigung | Mismatch between German address and US LLC “Principal Office.” | Use a Virtual Mailbox that offers a “Real Lease” in the US. |

| Norway | BankID Verification & DTAA | Sudden logins from “Non-EEA” IP addresses (like Peru or Vietnam). | Always use a Residential US IP before accessing BankID. |

| Ireland | PPS Number & Proof of Residency | Transfers to Irish “Neobanks” (like Revolut) exceeding €10,000. | Use Mercury for holding; use Wise only for the final conversion. |

| Canada | SIN Number & CRA Form NR301 | Failing to file Form 5472 (triggers a CRA/IRS data swap). | Link your IRS Form 5472 Guide as your primary defense. |

The “IP Address Trap”: Why Your VPN is a Compliance Landmine

In 2026, the biggest mistake a digital nomad can make is logging into a US bank account using a standard, commercial VPN. While services like NordVPN or ExpressVPN are great for Netflix, they are a massive “Red Flag” for banking AI.

The Mask vs. The Reality:

Think of a standard VPN like wearing a cheap, plastic mask to a high-security masquerade ball—everyone knows you’re hiding something. These services use Data Center IPs. Banks have a database of these addresses; when they see a login from a known data center, their automated security systems trigger a “Suspicious Activity” freeze instantly.

To stay under the compliance radar while moving between geopolitically stable hubs, you need to look like you never left home.

The Peak Strategy: Residential Proxies & Travel Routers

To pass a 2026 bank audit, your digital footprint must show a Residential IP. This is an address assigned to a real home in the US (like a Comcast or AT&T connection).

- The Pro Move: Use a Dedicated Residential Proxy (services like StarVPN or IPBurger). Unlike a shared VPN, this IP belongs only to you and never changes.

- The “Peak” Hardware: Serious nomads use a Beryl-AX (GL-MT3000) Travel Router. This allows you to hard-wire your laptop into a “VPN Tunnel” that stays connected to your US home base 24/7.

By using a residential footprint, you bypass the AI filters that catch 90% of other nomads, keeping your US Business Bank Account safe while you build your empire from the beaches of Peru or the cafes of Baku.

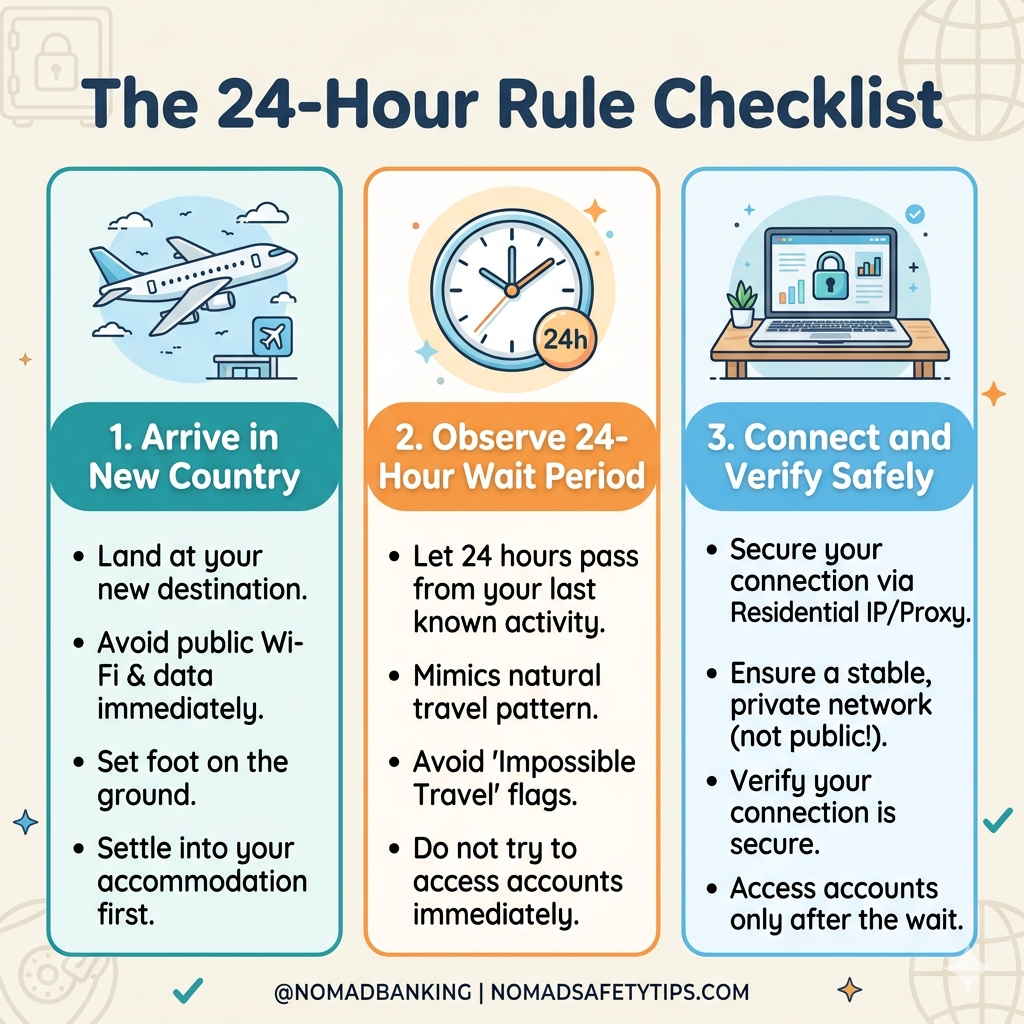

The “24-Hour Landing Rule”: Don’t Alert the AI

The most dangerous time for your US bank account is the moment your plane touches down in a new country. In 2026, bank security systems look for “Impossible Travel” flags—when a user logs in from New York at 10:00 AM and then from Lima, Peru, at 2:00 PM.

Even with a Residential IP, you should follow the 24-Hour Landing Rule:

- Digital Silence: Once you land, do NOT open your banking apps or PayPal on airport Wi-Fi. Airport networks are the highest-risk IPs in the world.

- Stabilize Your Connection: Wait until you are at your accommodation and your Travel Router or Dedicated Proxy is fully connected and tested.

- The “Slow Log-In”: Only access your bank after 24 hours have passed since your last login. This mimics a natural travel pattern and prevents the “geographic hop” trigger.

“Think your bank won’t notice you’re in Bangkok? With the new 2026 Thailand TDAC system now sharing data with global finance networks, your bank could see your digital arrival before you even leave the airport. If you don’t have your Residential IP active, your account could be flagged for ‘High-Risk Entry’ before you clear customs.”

By following this rule, you ensure that your US Tax Stack remains invisible to the compliance bots, allowing you to focus on your work instead of spending hours on the phone with bank support

Conclusion: Building a Crisis-Proof Banking Stack

In 2026, a US business bank account is no longer a “set-and-forget” asset. Between the Thailand TDAC monitoring and the global de-risking wave, your financial access is only as strong as your digital footprint. By implementing a Dedicated Residential IP, following the 24-Hour Landing Rule, and staying compliant with regional rules in Norway, Germany, and New Zealand, you ensure that your business remains operational while others are left stranded by “Shadow Freezes.”

Don’t wait for the “Account Restricted” email to arrive. Take control of your US Tax Stack today and anchor your business in stability, no matter where in the world you choose to wake up.

🚀 Secure Your US Banking Resilience Today

- Open a Mercury Business Account – Best for high-growth startups and tech nomads.

- Open a Relay Financial Account – Best for those who need multiple team cards and “Profit First” accounting.

- Connect to HubSpot CRM – The free way to automate your 2026 tax documentation and KYC history.

Why did Mercury or Wise freeze my business account

In 2026, most freezes are triggered by “Impossible Travel” flags or logins from known Data Center VPNs. Banks use AI to detect if you are accessing your account from a high-risk region without a Residential IP.

Q2: Can I use a standard VPN for US business banking?

Answer: No. Standard VPNs use shared IPs that are easily flagged by bank security filters. For 2026 resilience, you should use a Dedicated Residential Proxy or a hardware travel router.

Q3: Do I need to notify my bank before I travel?

Answer: While some banks suggest it, 2026 AI filters often ignore travel notices if your digital footprint looks suspicious. The “24-Hour Landing Rule” and a stable IP are your best defenses.